How to Set Up a Budget: A Simple Step-by-Step Guide

Take control of your money. Learn how to manage how to set up a budget, what is managing finances, make a budget and discover proven tips to save money ...

Money management is not something we are born knowing how to do; it is a skill we pick up along the way. Surprisingly, even though it is crucial for everything from our daily peace of mind to enjoying a carefree retirement, most folks do not get any formal training on what is managing finances or creating a sustainable cash flow system. This lack of knowledge often leads to widespread financial stress, living from paycheck to paycheck, and feeling like money is the boss of you. But here is the silver lining: the basics of how to handle money are simple, logical, and within reach if you are willing to learn. At the core of a successful financial life is one essential tool—the budget. When you get the hang of how to set up a budget, money stops being a source of stress and turns into a resource that helps you achieve your goals. In this guide, I will walk you through crafting a budget that works, delve into the philosophy of financial control, and offer practical strategies to make a budget you can stick with long-term.

A lot of folks avoid budgeting because they think it cramps their style. But actually, a budget is your ticket to true financial freedom. Think of it not as a cage, but as a map. Without a map, you are just wandering around and spending impulsively. With one, you can guide every dollar toward building the life you dream of.

What Is Managing Finances? A Comprehensive Definition

To really get a handle on how do you manage money, it is crucial to grasp the full scope of financial management. At its core, what is managing finances means strategically tracking income, allocating spending, cutting down debt, saving up, and investing any extra to reach specific life goals. It is way more than just math; it is about understanding human behavior, setting goals, assessing risks, and planning for the future. When folks ask how do you manage money, they are often looking for a simple recipe. But real money management rests on three pillars: awareness (knowing where every penny goes), control (spending intentionally), and alignment (making sure your spending mirrors your true values and priorities). A budget activates all three pillars.

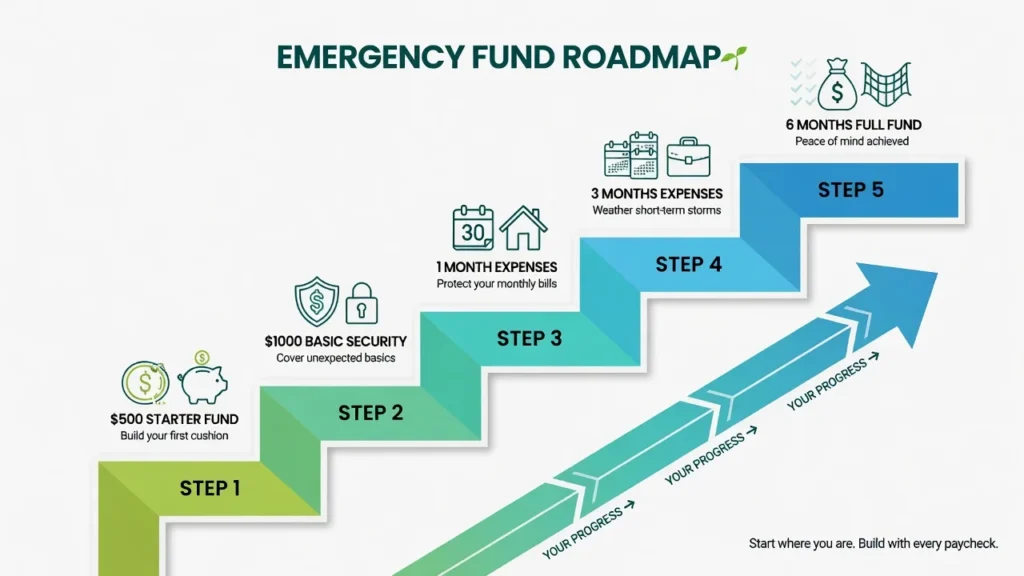

The Cost of Not Budgeting

Getting better at how to handle money better starts by recognizing the price of financial chaos. Without a budget, spending becomes reactive. You peek at your bank balance, see it is in the green, and figure you can make a purchase. But that balance does not consider upcoming bills, irregular costs, or savings goals. This leads to surprise expenses, credit card debt, and constantly feeling behind. Studies consistently find that people who do not budget tend to spend 15-20% more than they realize, simply because they are not tracking. This "invisible leak" is not about willpower; it is about lacking a system. Seeking help with budgeting is not admitting defeat—it is acknowledging that we are not naturally great at keeping track of numerous variable expenses monthly. You need a structured process.

- Plan your spending before the month starts: With zero-based budgeting, every dollar has a job before the month begins, so nothing goes to waste.

- Prepare for irregular expenses: Set aside funds for annual insurance premiums, car maintenance, and holiday gifts.

- Prioritize saving: Treat savings like a must-pay bill. Pay yourself first, before spending on non-essentials.

- Review and adjust monthly: Your budget should be a living document, not a rigid constraint.

- Check balance before each purchase: This is not planning; it is wishful thinking. A positive balance now does not cover rent due next week.

- Unexpected costs turn into debt: With no safety net, car repairs or medical bills end up on credit cards.

- Savings are an afterthought: Often, there is nothing left to save, so savings do not grow consistently.

- Dread checking bank accounts: Avoidance indicates a loss of control over cash flow.

How to Set Up a Budget: A Step-by-Step Framework

Setting up a budget can seem daunting, but it does not have to be. Follow these steps, and you will know how to budget my money effectively. When learning how to set up a budget, the process can be broken down into five discrete, repeatable steps.

Step 1: Calculate Your True Monthly After-Tax Income

Seems simple, but many people miscalculate what they actually have to spend. If you are salaried, use your monthly take-home pay after taxes, insurance, and retirement contributions. If your income varies (like freelance or commission work), average your income over the past six months to set a baseline. Extra income in good months goes to savings or debt, while you draw from a buffer in leaner months. To answer how do you budget your money with variable income, budget to your baseline and treat anything extra as a bonus.

Step 2: Track Every Expense for 30 Days (Without Judging)

Before crafting a budget, you must know where your money is going. Spend a month recording every expense, big or small. Use whatever works for you—a spreadsheet, notepad, or app. Do not change anything yet; just observe. At month's end, categorize each expense: fixed costs (rent, mortgage, insurance), variable necessities (groceries, utilities, transportation), and discretionary spending (dining out, entertainment, hobbies). Many people are surprised by how much goes to discretionary spending. This awareness is foundational for basic money management skills.

Step 3: Categorize and Apply the 50/30/20 Rule as a Starting Framework

One effective budgeting method to answer how to make a good budget is the 50/30/20 rule, popularized by Senator Elizabeth Warren. Allocate 50% of your after-tax income to Needs (housing, utilities, groceries, transportation, minimum debt payments), 30% to Wants (dining, entertainment, travel, hobbies), and 20% to Savings & Debt Acceleration (emergency fund, retirement investing, extra debt payments). Adjust these percentages based on your cost of living, but do not let essential costs eat up more than half your income. If they do, consider cutting costs or boosting income before building wealth.

Budgeting Methods: Choosing the Right Framework for Your Personality

There is no one-size-fits-all answer to how to budget my money. Different people thrive under different systems. The table below compares four of the most effective budgeting methodologies.